Mid-November 2015. It was time to negotiate the maze for signing up for health insurance through the health insurance marketplace (www.healthcare.gov). Am I a fan of the system? No and yes. Last year I had to sign up via phone (the website could not verify my identity). That was in Nov. 2014. My identity is now verified but I still cannot, a year later, access my 2015 application on the website. There is no explanation. So, imagine my angst when I went to sign up for my 2016 enrollment online. But, the system was merciful (or my karma was good this time, never question good fortune). My application went through smoothly. I heaved a sigh of relief.

Let me start by stating the obvious benefits of the Affordable Care Act (ACA) or sometimes known as Obamacare.

- Anyone can buy health insurance even without a job

- Nobody can be refused coverage even with preexisting conditions

- Young adults under 26 can stay on their parent’s plans

- No gender discrimination regarding pricing

- Many preventive services and some immunizations are covered at no additional cost

- Low income applicants get credits and can buy insurance at vastly reduced rates

- Upwards of 17.6 million people have gained health insurance

“Preventive services and early treatment are saving lives and we are thankful for those lives. People have longer, healthier lives with Obamacare” says Joanne Corte Grossi, Region 3 Director, U.S. Department of Health and Human Services, Philadelphia (Philadelphia Inquirer, Nov. 26, 2015).

Some of the arguments for implementing the ACA and having everyone insured were:

- It makes sense that everyone has access to health care and one does not have to wait till the last moment when illness has taken a real bad turn to visit the emergency room

- This is the norm in all developed countries (except the USA)

- It would make insurance cheaper since we now have a larger pool to insure especially the young who do not use or need health care that often.

The argument for lower rates has not generally panned out as anyone who has gone through the system this year will testify. Overall, I noticed a rise in premiums, a rise in deductibles and I learned also of the strange and disturbing term ‘balance billing’. Let’s say your doctor refers you to a hospital in your network for a procedure (e.g. surgery). You go through the procedure and later you get hit with a large unanticipated bill. It turns out the radiologist or anesthesiologist on call that day did not belong to your network and you have been billed for the balance, hence ‘balance billing”. It is perfectly legal, you are told. In case the egregiousness of the injustice is not clear, let me explain. You thought you had done your homework, gone to the proper hospital expecting everything to be covered after the copays and deductibles. But no, you now have to shell out cash, sometimes lots of it.

The way to fix this is to have healthcare systems that own the treatment as well as the insurance side of the business and have a comprehensive network of providers with whom contracts have been negotiated upfront. For the patient, this provides a ‘one stop shopping’ without the hassle of wondering if the physician, or surgeon he goes to belongs to his network or not. Frankly, this is the last thing a patient needs to worry about as he or she is being wheeled into an operating room. Providers like the Mayo Clinic and Geisinger are headed in the direction of a ‘one stop shopping’ network.

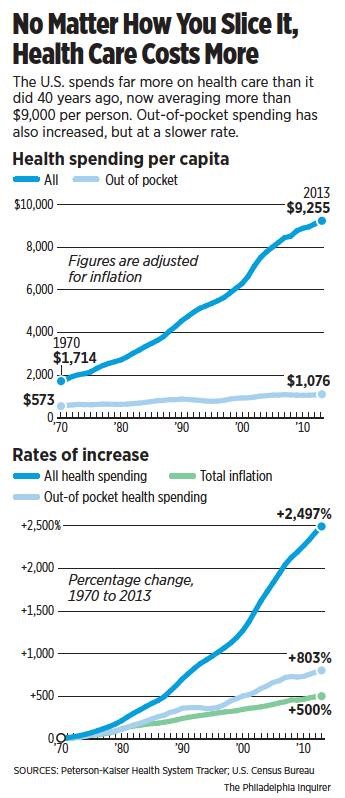

So why did the ACA not fulfill this expectation of lower cost? A glance at the graphs on the left may help answer this question. Don Sapatkin wrote an informative article ‘Diagnosis: Costly and Confusing’ in the (Philadelphia Inquirer, November 15, 2015), showing no matter how you look at it, healthcare is now costing more. From 1970 to 2013, the rate of increase of all health spending was 2497% while that of inflation and out of pocket health spending were just 500% and 803% respectively. This enormous increase in health care spending is absolutely unsustainable in the long run and has no relationship to inflation or rationally explainable health care costs. These costs are invariably pushed on to the patients, especially on the vulnerable elderly straining their meager budgets.

So why did the ACA not fulfill this expectation of lower cost? A glance at the graphs on the left may help answer this question. Don Sapatkin wrote an informative article ‘Diagnosis: Costly and Confusing’ in the (Philadelphia Inquirer, November 15, 2015), showing no matter how you look at it, healthcare is now costing more. From 1970 to 2013, the rate of increase of all health spending was 2497% while that of inflation and out of pocket health spending were just 500% and 803% respectively. This enormous increase in health care spending is absolutely unsustainable in the long run and has no relationship to inflation or rationally explainable health care costs. These costs are invariably pushed on to the patients, especially on the vulnerable elderly straining their meager budgets.

But why has the price of health care risen so high and what can the consumer do? They can shop around to get the best deal and stay informed. They can lobby their elected representatives to make meaningful changes to these laws, e.g. for more competition, but that will take time. One good way of controlling costs would have been the emergence of a single payer system against which the private insurances companies would have had to compete. That initiative was a non-starter from the get-go. Without the single payer system, we may have received the worst of both worlds. Everyone is now forced to buy insurance while the insurance companies can now arbitrarily raise prices, absent a genuine competition. Ditto for the rise in the price of drugs. Medicare is barred by law from negotiating the cost of drugs. Plus, mergers and acquisitions have led to fewer, larger companies that give them the market clout to set prices. For example, think of the planned mergers of Humana and Aetna or Pfizer and Allergan. This trend is good for the company share prices but not good for the end user.

What happens when there are only a few large providers? This is my take: Let us ‘follow the money’. The argument is often made that absent undue restrictions, competition and market forces will set prices of commodities. But health care is unique. When you are sick, you have to see a doctor and if you need a heart transplant, you either get a new heart or die. There is no other choice, unlike the case for say, buying a new dress or TV, where you can wait or forego if you cannot afford it. In this scenario, there is the temptation to keep on raising prices, knowing that the patient has no option but to pay. No one is against an acceptable rate of return or profit, but what is an ‘acceptable rate’? It is a tough question, which we as a society, have to answer. But let us look at the lower graph again. Is 2497% increase in spending over 43 years ‘acceptable or justifiable’? This trend will bankrupt us if left unchecked. Therefore, a case can be made for more competition and reasonable oversight to rein in the runaway cost increase.

At a more granular level, the cost of completing medical school is now very high. Hence, doctors are hundreds of thousand dollars in debt when they graduate. They need to recoup as fast as possible. In the present system, payments are based on number of procedures or treatments, which leads unfortunately to many unnecessary tests, treatments and medications. All these add to the increase in health care spending. Making medical school more affordable, lowering the price of drugs by importing cheaper medicines made in other countries, allowing Medicare to negotiate prices of drugs and taking a more holistic view emphasizing disease prevention are some of the ways to reduce health care costs. The Cleveland clinic is taking such an approach with incentives to keep patients healthy and out of the hospital.

For the moment, I am glad that I was able to complete my 2016 health care application online without trouble and will do what I can to stay healthy throughout the year. I will discuss how patients can take a more active part in their own health care in future posts.

Ranjan Mukherjee Ph.D. is a scientist, writer, speaker.

Very detailed. Agree the system’s not perfect, but a step in the right direction. Wish all states would have jumped in completely, and I think a public option would keep things more competitive.

LikeLike